QUARTERLY FINANCIAL RESULTS

LEXICON BANCORP REPORTS CONSOLIDATED FINANCIAL RESULTS FOR THE THREE MONTHS ENDED MARCH 31, 2025

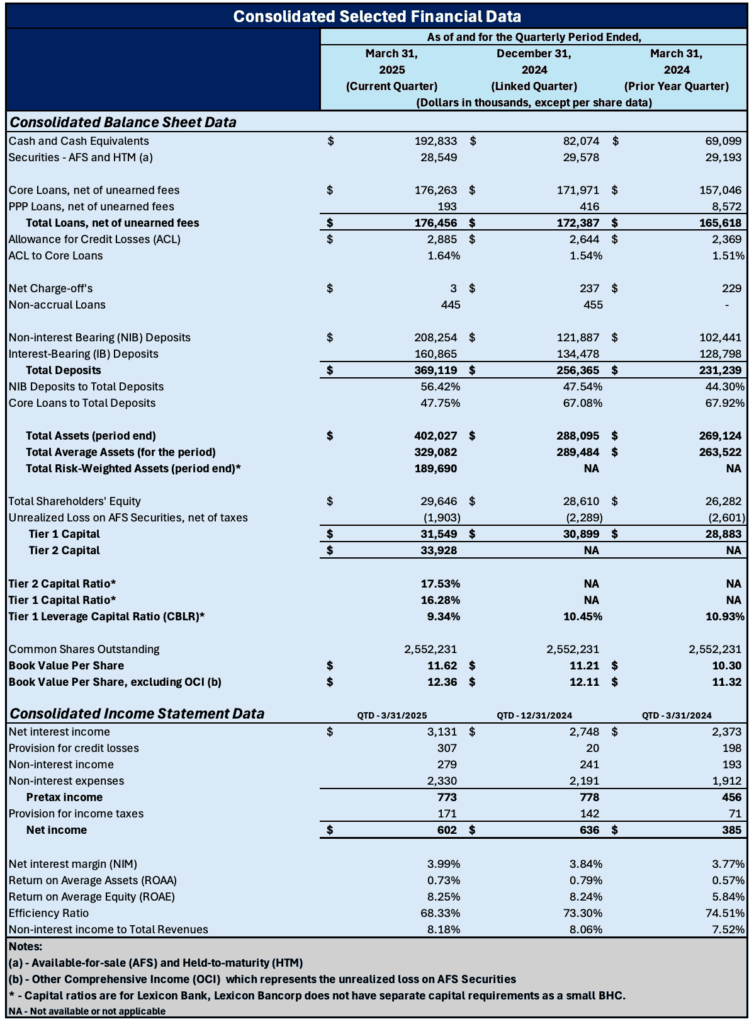

Key Highlights

- Net income of $602 thousand this quarter; up 56.36% over the $385 thousand for the quarter ended March 31, 2024

- Core loans grew to $176.3 million, up 2.50% from last year

- Total deposits grew to $369.1 million, up 43.98% from last year

- Non-interest bearing deposits were 56.42% of total deposits

- Total assets increased to $402.0 million, up 39.55% from last year

- Strong on-balance sheet liquidity sources with cash and cash equivalents of $192.8 million and investment securities of $28.5 million

- Book value per share grew to $11.62, up 3.62% from last year

Lexicon Bancorp (“Bancorp”), the parent company for Lexicon Bank (“Bank”) (collectively, “the Company” or “Lexicon”), announces unaudited consolidated financial results as of and for the three months ended March 31, 2025. Lexicon continues to focus on personalized concierge banking services for clients, reflected in the year-over-year increase in net income driven by the continued growth in core loans and deposits.

"Lexicon Bank continues to leverage and further build upon our momentum from 2024 through the first quarter of 2025, delivering strong financial results driven by our commitment to personalized service, disciplined growth, and sound balance sheet management," said Stacy Watkins, President and CEO of Lexicon Bank. "Our growth in assets, deposits, and shareholder value reflects the strength of our foundation and the trust our clients and investors place in us. With a resilient and diversified deposit base, robust liquidity, and another 5-star rating from BauerFinancial, we are proud to remain a stable and forward-looking financial partner for our community."

"While there is broader economic uncertainty, Lexicon Bank’s long-term, relationship-driven approach positions us to navigate changing conditions confidently. We remain steadfast in our mission to support our clients, community, and shareholders—focused not on reacting to short-term volatility but building lasting value through strength, stability, and service."

For the three months ended March 31, 2025, net income was $602 thousand compared to $385 thousand for the three months ended March 31, 2024. The results were driven by the following changes:

- Higher net interest income by $758 thousand driven by continued balance sheet growth

- Increased provision for credit losses by $109 thousand driven by loan growth and continuing to build the allowance for credit losses given the current economic uncertainties

- Higher non-interest income by $86 thousand primarily from continued growth in client deposit accounts and a $31 thousand increase in the earnings from the Bancorp’s noncontrolling equity investment in IconTrust, a Las Vegas based trustee services provider

- Increased non-interest expenses by $418 thousand, attributable to increased salaries and benefits, marketing/sponsorships and technology costs.

Lexicon’s annualized return on average assets and return on average equity for the three months ended March 31, 2025, improved to .73% and 8.25%, up from .57% and 5.84% from a year ago, respectively, moving us closer to our strategic goals of 1% and 10%, respectively.

Core loans, net of fees, grew to $176.3 million as of March 31, 2025, reflecting net growth of $19.2 million, or 12.24%, from March 31, 2024, and demonstrating our support for the businesses who are building and investing in the Southern Nevada community. The core loan portfolio continues to perform well, remaining healthy and strong, nonaccrual loans totaled $445 thousand at March 31, 2025. The allowance for credit losses to total core loans was 1.64% on March 31, 2025, compared to 1.51% on March 31, 2024.

PPP loans, net of fees, decreased to $193 thousand during the quarter compared to $8.6 million on March 31, 2024, primarily from the continued forgiveness of the loans.

Total deposits were $369.1 million on March 31, 2025, with non-interest bearing deposits improving to 56.42% of total deposits from 44.30% a year ago. We continue to remain focused on building relationships, many of which are primarily deposit focused, and utilizing third parties to expand FDIC deposit insurance coverage for larger relationships when desired. Deposits are expected to decline as a portion of this quarter’s growth reflected certain temporary deposits placed with the Bank.

Our core loan-to-deposit ratio was 47.75% on March 31, 2025. We continue to leverage our deposit base through the origination of core loans, seeking to move the ratio closer to 80% over time as we serve the needs of businesses in Southern Nevada.

We held cash and cash equivalents of $192.8 million, or 52.20% of total deposits, on March 31, 2025. Additionally, we have combined unused lines of credit and unpledged securities totaling $106.0 million, or 28.72% of total deposits, on March 31, 2025. The combined cash and cash equivalents, unused lines of credit and unpledged securities represent approximately 81% of total deposits. This combination of liquid assets and available resources provides a strong liquidity position for Lexicon and our clients.

Total shareholders’ equity was $29.6 million on March 31, 2025, compared to $26.3 million on March 31, 2024, driven by net income and a decrease in the net unrealized losses on available for sale (“AFS”) securities by $698 thousand, which totaled $1.9 million on March 31, 2025, compared to $2.6 million a year ago.

Lexicon’s Tier 2 Capital Ratio was 17.53% (10% required to be well-capitalized), Tier I Capital Ratio was 16.28% (8% required to be well-capitalized) and the Tier I Leverage Capital Ratio was 9.34% (5% required to be well-capitalized). Tier 1 and Tier 2 Capital totaled $31.55 million and $33.93 million, respectively, on March 31, 2025.

As of March 31, 2025 Lexicon’s consolidated total assets were $402.0 million, an increase from $113.9 million on December 31, 2024, driven by the growth in deposits used to fund the increase in the core loan portfolio and on-balance sheet liquidity.

Presented below is a summary of the Consolidated Selected Financial Data as of and for the periods indicated:

ABOUT LEXICON BANCORP

Lexicon Bancorp was established in July 2023 to become the bank holding company for Lexicon Bank. Founded in 2019, Lexicon Bank is Southern Nevada's community-focused banking partner. Lexicon provides personal, comprehensive banking services to business and individual banking clients, emphasizing creating and nurturing long-term relationships. By providing personalized services to all clients, Lexicon helps to foster Southern Nevada's economy and community—ultimately helping to grow and develop the region's local businesses. The Bank is redefining banking as it should be in Southern Nevada by creating a concierge-like experience for businesses, regardless of size. Lexicon Bank is located in Tivoli Village at 330 S. Rampart Blvd., Suite 150. The Bank is open from 9 A.M. to 5 P.M. Monday through Friday and 9 A.M. to 12 P.M. on Saturdays. Clients can contact us by phone at 702.780.7700 or online at lexiconbank.com. Follow us on Facebook, Instagram, LinkedIn, and X. Lexicon Bank is a member of the FDIC.

This press release includes “forward-looking statements,” as such term is defined in the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on the current beliefs of the Company’s Board and executive officers (collectively, “Management”), as well as assumptions made by and information currently available to the Company’s Management. All statements regarding the Company’s business strategy and plans and objectives of Management of the Company for future operations are forward-looking statements. When used in this press release, the words “anticipate,” “believe,” “estimate,” “expect” and “intend” and words or phrases of similar meaning, as they relate to the Company or the Company’s Management, are intended to identify forward-looking statements. Although the Company believes that the expectations reflected in such forward-looking statements are reasonable, it can give no assurance that such expectations will prove to be correct. Important factors that could cause actual results to differ materially from the Bank’s expectations (“cautionary statements”) are the effects of the COVID-19 pandemic and related government actions on the Company and its clients, loan losses, changes in interest rates, loss of key personnel, lower lending limits and capital than competitors, regulatory restrictions and oversight of the Company, the secure and effective implementation of technology, risks related to the local and national economy, the Company's implementation of its business plans and management of growth, loan performance, interest rates, and regulatory matters, the effects of trade, monetary and fiscal policies, inflation, the effects of natural disasters, and changes in accounting policies and practices. Based upon changing conditions, if any one or more of these risks or uncertainties materialize, or if any underlying assumptions prove incorrect, actual results may vary materially from those described as anticipated, believed, estimated, expected, or intended. The Bank does not intend to update these forward-looking statements.